![$adHeader[0]['title']](https://bfisnews.com/images/bigyapan/1776181672_1100 x100.gif)

NIC Asia Maintains Strong Balance Sheet, Interest Income Leads Growth

- BFIS News

- 2026 Mar 14 18:50

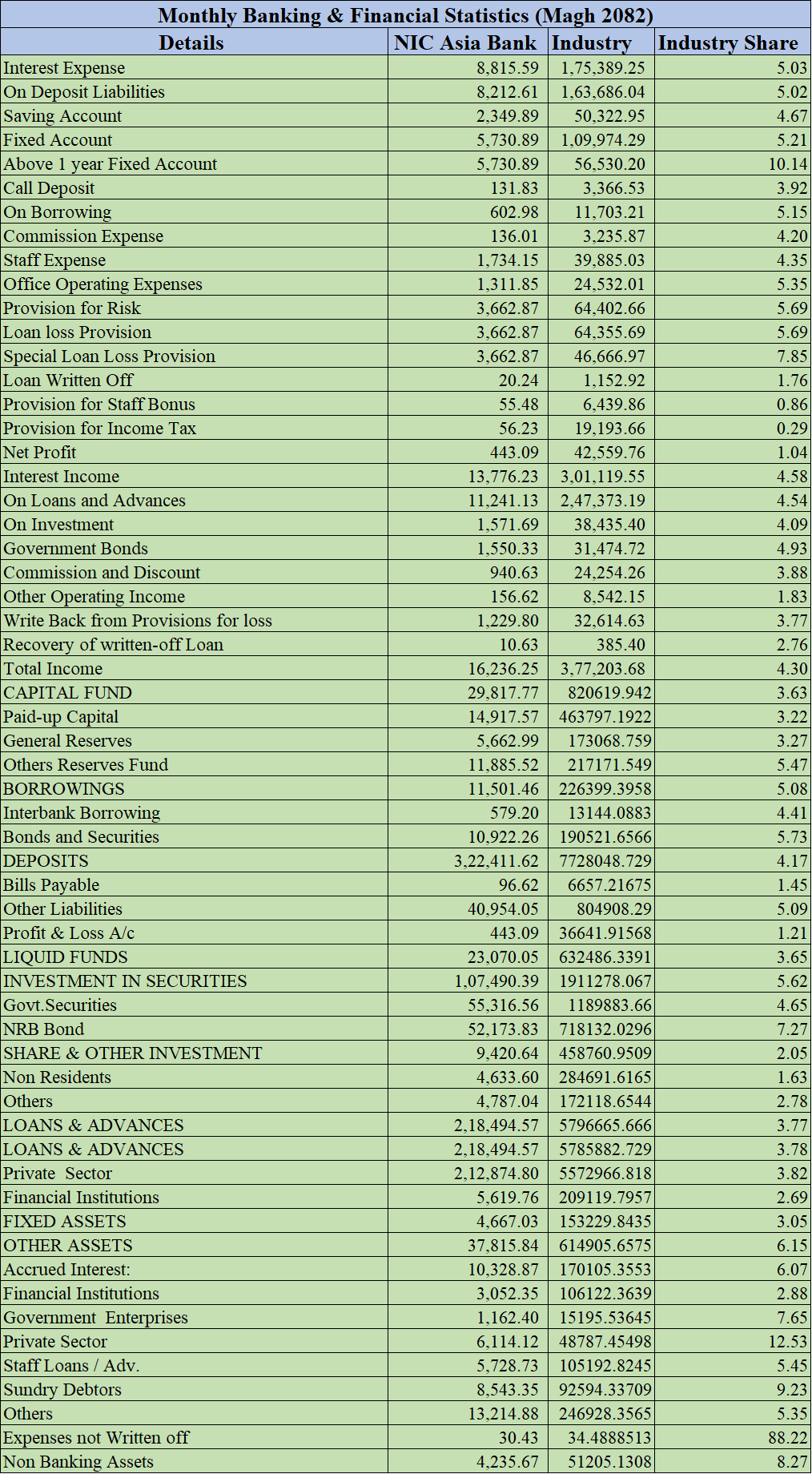

Kathmandu: NIC Asia Bank has reported a net profit of Rs 443.09 million, accounting for roughly 1.04 percent of the total profit generated by Nepal’s banking industry, indicating moderate profitability relative to the bank’s large balance sheet. Despite strong lending and deposit mobilization, operating costs and provisioning expenses continue to place pressure on the bank’s overall earnings performance.

Interest Income Remains Key Driver

Interest income remains the bank’s primary source of revenue, totaling Rs 13,776.23 Million, which represents about 4.58 percent of the industry’s total interest earnings. Loans and advances contributed the largest share, generating Rs 11,241.13 Million, roughly 4.54 percent of the sector’s lending income, highlighting the bank’s strong credit exposure and active lending operations.

Income from investments reached Rs 1,571.69 million, largely driven by returns from government securities and bonds issued by Nepal Rastra Bank.

However, the bank’s interest expenses stood at Rs 8,815.59 million, exceeding 5 percent of the industry’s total interest costs. Fixed-account deposits alone accounted for Rs 5,730.89 million, indicating the bank’s heavy reliance on relatively high-cost deposit products, while call deposits contributed only a minor share.

Operating Costs and Risk Provisions

The bank reported staff expenses of Rs 1,734.15 million, equivalent to 4.35 percent of total industry staff costs, reflecting moderate investment in human resources. Office operating expenses reached Rs 1,311.85, contributing 3.47 percent to the sector.

Provisioning for potential loan losses remained a significant cost, totaling Rs 3,662.87 million, which represents around 5.69 percent of the industry’s provisioning expenses. Analysts say this reflects a cautious approach to credit risk management but also reduces short-term profitability.

Loan Recovery and Asset Quality

Loan-loss provisions made up the entire provisioning charge during the period, with no special loan-loss provisions recorded. Recoveries from previously written-off loans remained relatively low at Rs 10.63.

However, write-backs from previous provisions totaled Rs 1,282.80 million, suggesting either improved asset quality or conservative provisioning practices in earlier periods.

Capital and Deposit Strength

The bank’s capital fund stands at Rs 29,817.77 million, accounting for 3.63 percent of the total banking industry capital base. Paid-up capital forms roughly half of this amount, supported by general reserves and other reserve funds.

Deposits reached Rs 3,22,411.62 million, representing around 4.17 percent of industry deposits, underscoring the bank’s strong presence in deposit mobilization. Borrowings remain moderate at Rs 11,501.46 million.

Lending and Investment Portfolio

Total loans and advances amount to Rs 2,18,494.57 million, or 3.76 percent of the banking sector’s total lending. The majority of lending is directed toward the private sector, while exposure to other financial institutions remains minimal.

The bank also maintains a significant investment portfolio of Rs 1,07,490.39 million, representing 5.62 percent of industry investments, with government securities and bonds issued by Nepal Rastra Bank forming the core of the portfolio.

Liquidity Position

NIC Asia maintains a stable liquidity profile, with liquid funds totaling Rs 23,070.05 million, about 3.65 percent of the industry’s liquid assets.

Other assets amount to Rs 37,815.84 million, including accrued interest, staff loans, sundry debtors, and claims on financial institutions. Non-banking assets remain small, indicating minimal stress from collateral takeovers.

While NIC Asia Bank continues to maintain strong deposit growth and a sizable investment portfolio, analysts note that high interest costs and significant provisioning expenses continue to limit profitability. Going forward, improved asset quality and better cost efficiency could help strengthen the bank’s earnings performance.

शेयर गर्नुहोस

प्रतिक्रिया दिनुहोस्

सम्बन्धित समाचार

_jEGOtGcTjV.jpg)

प्रतिक्रिया